Welcome to Capital Call: A OneFund Newsletter

A bi-weekly newsletter from LPs for LPs, covering the latest and greatest from across the private markets

Welcome and thanks for joining me (John Bailey, Co-Founder at OneFund) for the first edition of Capital Call, a newsletter for LPs, by LPs. We’ll be releasing this newsletter bi-weekly to our subscribers and those already using OneFund.

While there are lots of PE and VC newsletters out there, we are specifically writing this newsletter for current and aspiring PE and VC fund investors (also known as Limited Partners or LPs).

Our goal with Capital Call is to provide a high-quality, bite-sized digest on the latest insights, updates, and thought leadership from across the private markets.

As OneFund works to grow access to private market investment opportunities, we strongly believe that increasing knowledge of private markets for potential investors is equally important.

Here’s what we plan to cover in the newsletter:

Market Trends & Data: I’ll share insights and data from sources that leading institutional investors use to make investment decisions. This will give a sense of how investors cut through the noise and where opportunities may exist for LPs to deploy capital.

Deals & Fundraising: It’s too hard to keep up with the entire industry so I’ll cover the most noteworthy fundraises, private market reports, and how they impact LPs.

GP Perspectives: Thought leadership from industry GPs so you can understand how they are making sense of the market.

Subscribe now and stay ahead of the curve with OneFund.

Private Market Chatter

McKinsey Private Markets Outlook

Late last month, McKinsey released their 2023 private markets outlook. The title “Private markets turn down the volume” highlights a theme across private markets as it slowly but surely caught up to the downturn in public markets. That being said:

Private markets outperformed public markets on the way down, whether due to truly more resilient portfolios, a lag in timing, or manager discretion over their marks. - McKinsey

We spent the past few days diving right into the 74-page report to distill relevant trends and insights that matter most to LPs.

Fundraising Struggles: A Disproportionate Impact on Emerging Managers

2022’s fundraising headwinds did not affect all managers equally. In the turbulent market, LPs have been cautious to deploy capital to emerging managers and flocked to more established funds.

According to the report, funds greater than $5 billion raised a record $445 billion, 51 percent more than in 2021. On the other hand, funds smaller than $1 billion raised just $349 billion, a decrease of 31 percent.

Record amounts of capital are moving to managers with the largest track record which is not surprising given the market uncertainty. The top 20 fundraisers raised 32 percent of the total fundraising volume in 2022, which is the highest share since 2009 and a 9 percent year-over-year increase.

First-time fund fundraising fell to $32 billion, the lowest total since 2013 and the lowest share of total fundraising in at least 20 years.

How do we think through this?

At OneFund, we focus to partner with experienced managers which can help get one more comfortable with their investing capabilities. The capital deployment trends from 2022 have only reinforced that sentiment.

For LPs, the decision shouldn't be as simple as running to the largest managers. Be sure to consider the track record of the individual managers themselves, their strategy, and the consistency of returns.

Often smaller funds can tick these boxes and given their recent fundraising trouble, it could represent an opportunity for out-sized returns if one picks the right fund - although it can be a risky proposition.

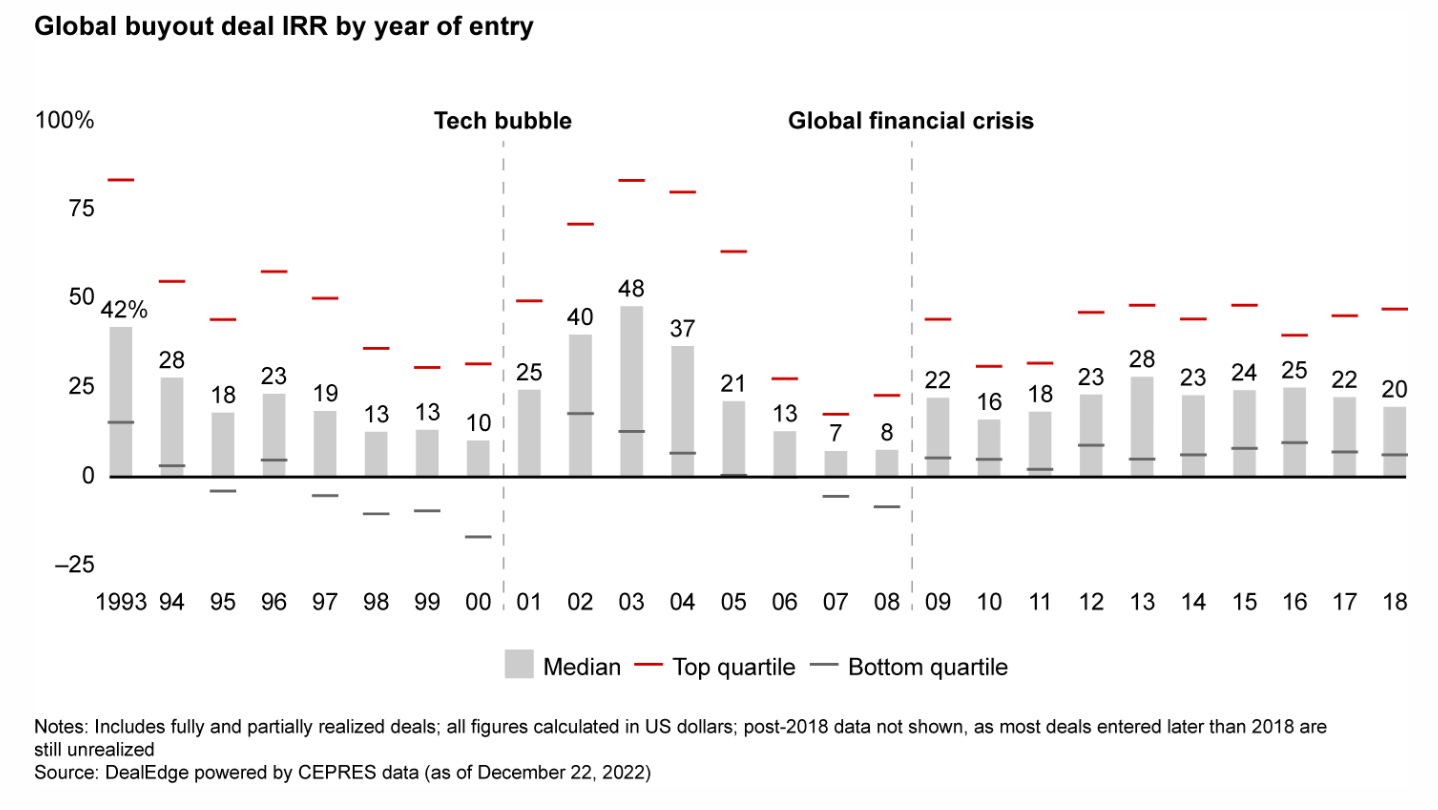

Interestingly, data from Bain’s Global Private Equity Report indicates a potential opportunity with buyout funds as they have historically tended to generate stronger returns coming out of recession when compared to the years going in. Global buyout IRR saw spikes coming out of both the 2001 tech crash along with the 2008 financial crisis.

Non-Institutional Capital Comes into Focus

A running theme that various industry reports have highlighted is the demand for non-institutional capital. Not only did McKinsey allocate an entire section to the subject, but Bain’s recent Global PE report noted the priority amongst GPs to tap further into individual investors. As alternative asset classes reach saturation within the institutional investor pool, the next frontier lies within individual investors.

At present, retail investor allocations to private markets are very low, ranging from 5–6 percent, but there is a big desire from GPs to grow this number.

As more institutional investors achieve asset-allocation maturity and slow the growth of their new commitments to private markets, non-institutional capital will be the next growth frontier for GPs. - McKinsey

Not to mention, investing in the private markets appeals to non-institutional investors for the same reasons that it does to institutional ones:

The potential for higher returns

Lower correlation with public equity markets

Access to otherwise inaccessible markets and strategies

If you enjoyed this read and have any questions or would like to discuss further, feel free to schedule a call with us - we’re happy to chat.

Updates from Across the Ecosystem

Fundraising

📈 KKR set for Q3 Fund V launch targeting $20bn

VC & PE Reports

🔬 Bain Global Private Equity Report 2023

🔬 PitchBook Analyst Note: The Collapse of Silicon Valley Bank

🔬 Blackrock 2023 Private Markets Outlook

GP Perspectives

In each newsletter, I plan to share perspectives from thought leaders across the venture and PE ecosystem. We spend time scrolling for insights from some of the most successful capital allocators so you don’t have to.

Here’s what we came across this week 👇

Gavin Baker (CIO, Atreides Management)

Gavin points to the current illiquidity discount in some facets of the private markets, a first in the past 10 years. This is an interesting opportunity for LPs looking to deploy long-term capital in private markets.

David Sacks (Partner, Craft Ventures)

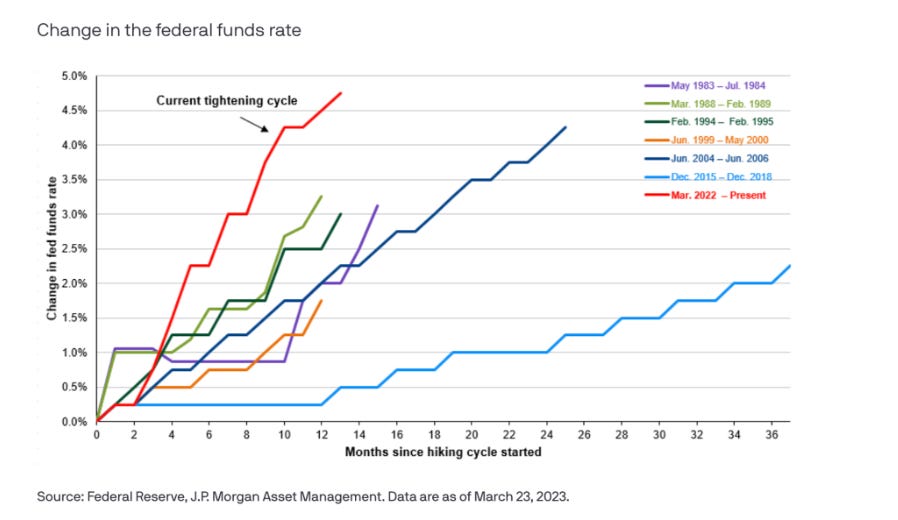

Sacks, also a co-host of All In, shares his thoughts on the first and second-order impacts of the Fed rate hikes:

Compared to past tightening cycles, rates have risen to very high levels in a very short period of time…

Chamath Palihapitiya (CEO, Social Capital)

There are a lot of potential risks of a ‘heard mentality’ in venture investing. For LPs allocating capital, factors like correlation and DPI should be increasingly top of mind, because running with the crowd may not be the safest strategy after all. Often some of the greatest return profiles in venture were originally the most contrarian bets. When the crowd tends to zig in terms of what they invest in, it can often help to zag.

About OneFund

We’re democratizing access to Private Equity and Venture Capital for everyday investors. We partner with the world's top PE & VC funds to offer investment options without the million-dollar minimums.

If you would like to follow what we are doing, get more regular updates directly from the team, or access to the platform, you can join our waitlist below!